.png)

July 8, 2026 | EIA Data: Week Ending July 6, 2026 | NWS Data: July 7, 2026 | AHX Platform Data: July 7, 2026

Six weeks down. Every region. Again.

The streak is real, but this week the headline isn't the direction — it's the cumulative result and what it means for your transport costs. The Midwest has fallen $1.36/gal over eight weeks from the May spike peak. That's a 23.3% decline from a high that had carriers stretched thin and shippers absorbing costs they hadn't budgeted for. The spring fuel crisis is definitively behind us.

The big story this week is what's happening on the ground: the market is back from the July 4th holiday, the flooding that dominated the center of the country for six weeks has dramatically improved, and wildfire season has peaked on the West Coast.

Here's everything you need to know.

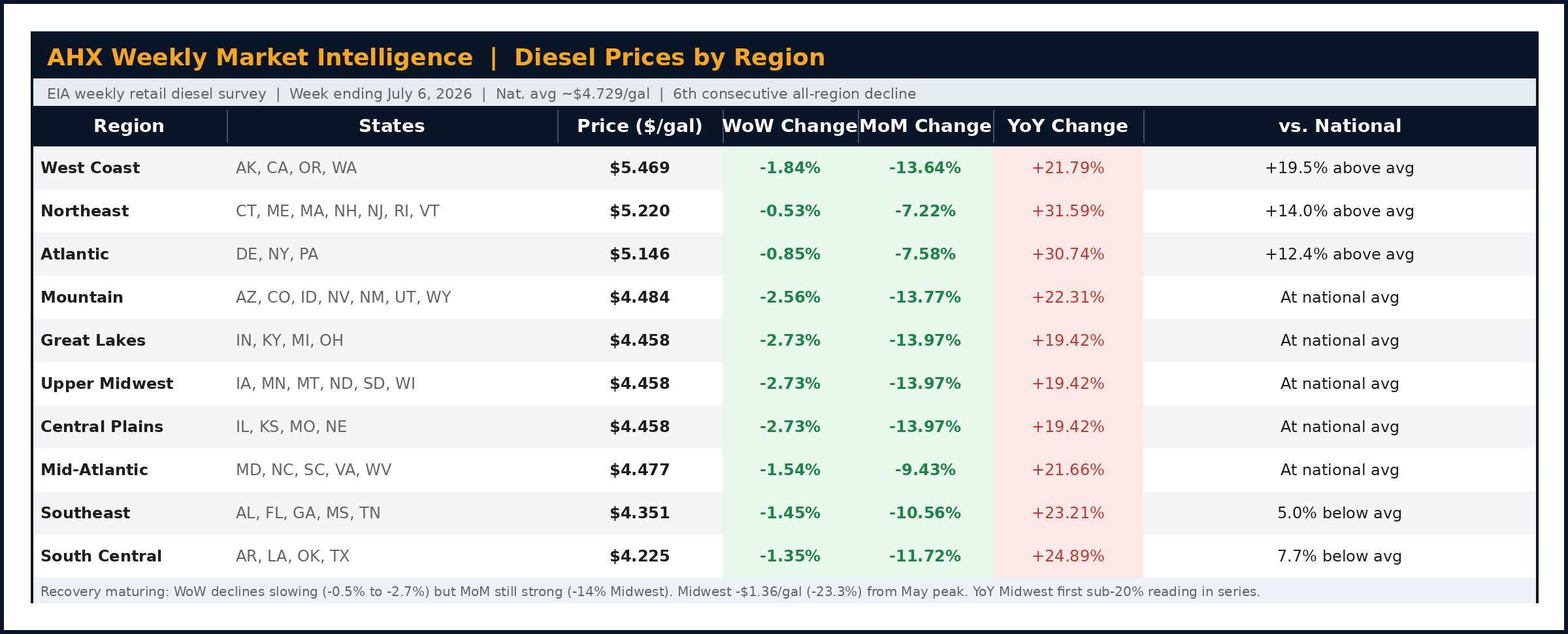

Diesel Prices by Region — Week Ending July 6, 2026

Six Weeks Down: The Cumulative Picture

This is the sixth consecutive week every region has declined. The weekly moves are smaller this week — the recovery is maturing — but the cumulative math is the story worth telling.

From the May peak: The Midwest has fallen $1.357/gal, a 23.3% decline, over eight weeks. The West Coast has dropped $1.455/gal, a 21.0% decline, from its April high. South Central has come down $1.190/gal, a 22.0% decline, from its peak.

The month-over-month view is particularly compelling right now. Great Lakes, Central Plains, and Upper Midwest are all at -13.97% MoM. West Coast is at -13.64% MoM. These are meaningful 30-day moves that translate directly into lane pricing adjustments. If you haven't run a fresh market estimate in the past few weeks, you're working with a number that's meaningfully stale.

YoY compression has reached a notable milestone. The Great Lakes, Central Plains, and Upper Midwest are now at just +19.42% year-over-year — the first time any region has been below 20% above last year's price since the spring escalation began. The Mid-Atlantic is at +21.66% YoY. These are the best year-over-year comparisons in this entire series.

The structural reality hasn't changed: diesel is still more expensive than it was in 2025. But the narrative has shifted from "costs are still rising" to "the recovery has been sustained and material."

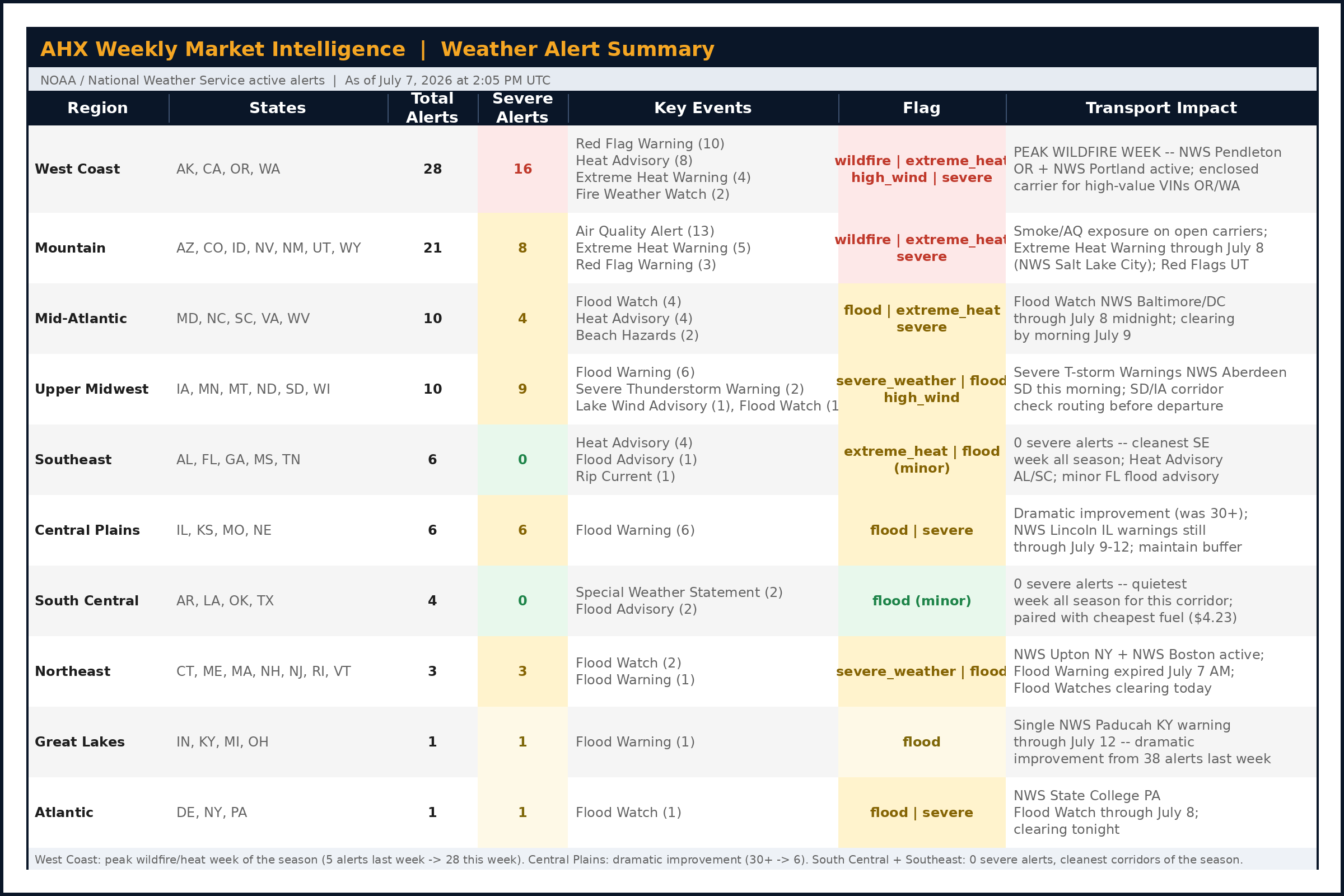

Weather Alert Summary — July 7, 2026

The Weather Story: The Flooding Abates, the West Coast Ignites

Six weeks ago, the Central Plains had 57 active weather alerts. Last week it had 30. This week it has 6. The flooding that gripped the center of the country from early June through late June has dramatically de-escalated — a meaningful improvement for the I-70 and I-55 corridors that have been compromised since before Memorial Day.

The weather story this week has moved decisively west.

West Coast: Peak Wildfire and Heat Risk of the Season

The West Coast went from 5 total alerts last week — the quietest corridor in the country — to 28 alerts with 16 rated severe this week. That is the most dramatic single-week weather escalation we've tracked in this series.

Ten Red Flag Warnings are active across Oregon, Washington, and California, issued by NWS Pendleton OR, NWS Portland, NWS Sacramento, and NWS Seattle. Four Extreme Heat Warnings and two Fire Weather Watches round out the picture. This is the highest wildfire risk week on the West Coast all season, and it arrives at the same time as extreme heat conditions — a combination that can produce rapid, unpredictable fire activity.

For vehicle transport: Red Flag conditions mean any fire that ignites can spread rapidly, closing highways with little notice. Interstate 5 (OR/WA), US-101, and I-80 are the most likely routes to be affected. For standard open-carrier shipments, request a carrier check-in at both pickup and delivery. For high-value, collector, or condition-sensitive vehicles routing through Oregon or Washington this week, enclosed carrier is the right choice.

Mountain: Air Quality and Heat

The Mountain corridor has 21 alerts, 8 severe — 13 Air Quality Alerts from regional wildfire smoke, 5 Extreme Heat Warnings through July 8, and 3 Red Flag Warnings from NWS Salt Lake City. The air quality picture makes this a meaningful open-carrier consideration: smoke-heavy conditions leave fine residue on vehicles in transit. For high-value vehicles routing through AZ, CO, NM, or UT, note vehicle condition at pickup and consider enclosed carrier if smoke conditions are severe.

Upper Midwest: Severe Thunderstorms This Morning

NWS Aberdeen, SD issued Severe Thunderstorm Warnings this morning alongside 6 Flood Warnings and a Flood Watch. The SD/IA/WI corridor has elevated risk today specifically. Most of the severe thunderstorm risk should clear through the day. Check routing through South Dakota and northern Iowa before dispatching.

Mid-Atlantic: Flood Watch Through Tonight

NWS Baltimore MD/Washington DC issued a Flood Watch through midnight July 8 EDT — meaning it's active at the time of publication but should resolve by early July 9. If you have Maryland or Virginia shipments with same-day or next-morning pickups, check current NWS conditions before confirming departure.

Central Plains and Great Lakes: The Great Improvement

Six weeks of persistent severe flooding have finally begun to lift. Central Plains: 30+ alerts last week → 6 this week. Great Lakes: 38 → 1. This does not mean the long-duration Flood Warnings have lifted — NWS Lincoln IL has Flood Warnings running through July 9 and July 12 — but the acute, broad-based flooding crisis has passed. The I-70/I-55 corridor is moving toward normalization.

South Central and Southeast: The Best Weather Corridors of the Season

South Central has 4 total alerts, zero severe. Southeast has 6 total alerts, zero severe. Both regions have been dealing with one weather threat type or another since early spring. This week, for the first time in months, both are effectively clear. Combined with the lowest fuel prices in the country in South Central ($4.225/gal), these are the two most favorable execution corridors in the country right now.

What the AHX Platform Is Showing

The market held through the July 4th holiday and is now rebounding. The Carrier Market held steady across every single day from July 1 through July 7 — including through the holiday itself. Volume direction, which went into holiday-driven decline through July 3–6, is now normalizing. The 7-day rebound is underway, consistent with the post-holiday recovery pattern we observed after Juneteenth.

Georgia holds the #1 pickup market position for the seventh consecutive week. At this point that's not a weekly observation — it's a sustained market reality. The Atlanta metro auction ecosystem and Southeast dealer density make Georgia a consistently high-activity origin for the platform. Dealers sourcing in Georgia have found carrier availability healthy all summer.

Ohio is this week's strongest accelerating market, posting solid positive momentum on both pickup and delivery simultaneously. Kansas, Virginia, and North Carolina are all showing sustained pickup strength. On the delivery side, Minnesota leads followed by Michigan and Nebraska.

The lane supply picture heading out of the holiday is healthy. Carrier coverage is broad, conditions are favorable, and the market is active. Use the AHX Market Estimate Tool before every post — six weeks of fuel relief mean lane estimates have adjusted meaningfully from where they were in May.

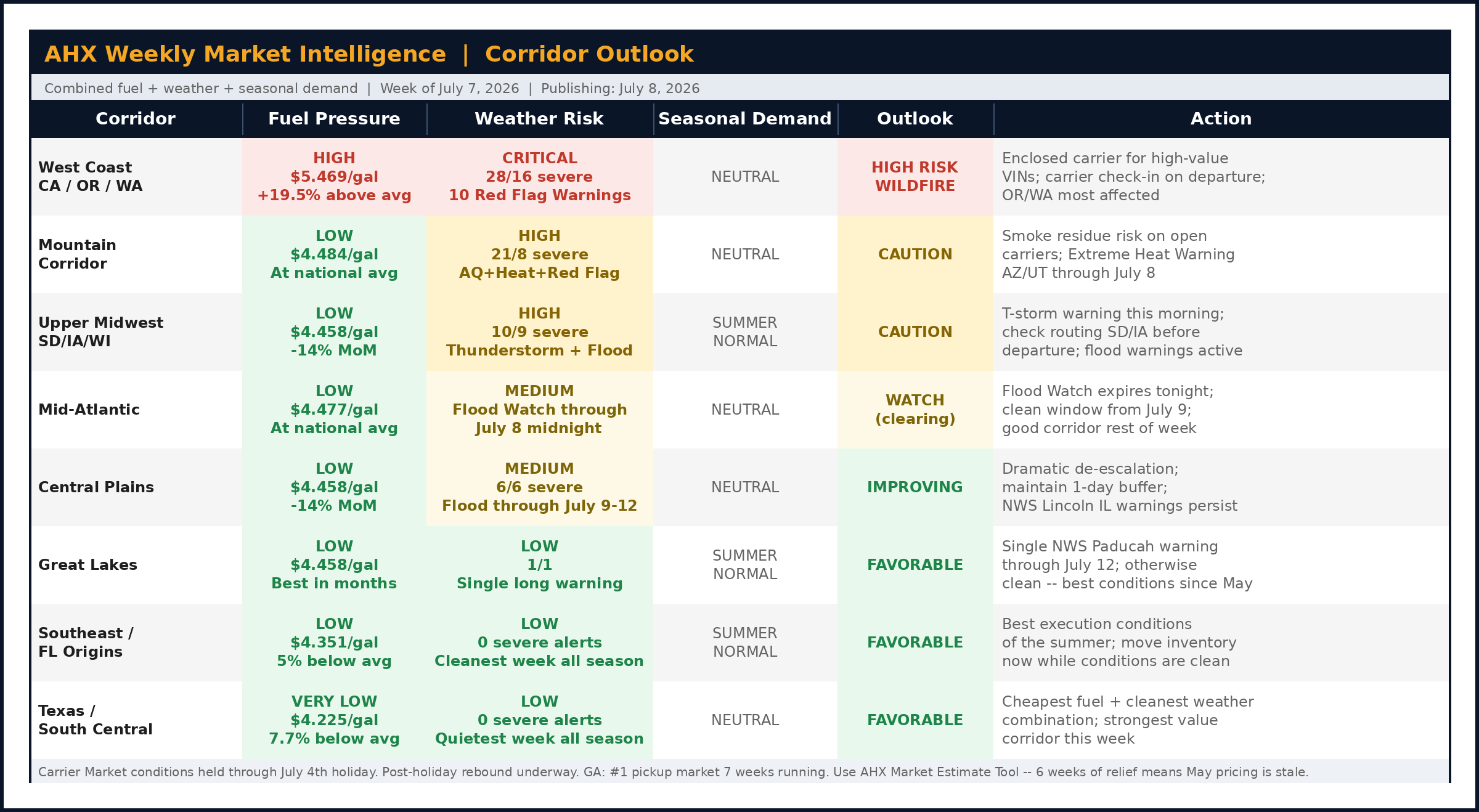

Corridor Outlook for the Week

West Coast: Peak wildfire and heat risk week of the season. Open-carrier moves through OR and WA need carrier check-in protocols. High-value vehicles deserve enclosed carrier consideration. Fuel has improved materially (-21% from April peak) but the California premium persists at +19.5% above national average.

Mountain: Air quality and heat story rather than direct fire risk for most of the corridor, though Red Flag Warnings are active in UT. Smoke residue risk for open carriers. Enclosed carrier appropriate for high-value VINs routing through AZ, CO, or NM.

South Central: The best combination of any corridor this week — cheapest fuel in the country, zero severe weather alerts, and healthy carrier coverage. If you have vehicles sourced in Texas or the Gulf Coast, this is a favorable week to move them.

Southeast / Florida: Similar to South Central — zero severe alerts, affordable fuel ($4.35/gal), and improving carrier flow. The summer baseline for this corridor is healthy.

Central Plains: Long-duration Flood Warnings from NWS Lincoln IL run through July 9–12. Build a buffer into routing through IL/KS/MO. The overall picture is dramatically improved but those specific warnings haven't lifted.

Mid-Atlantic / Atlantic: Flood Watch resolves tonight (July 8). By the time this publishes, conditions should be clearing. Good corridor for the rest of the week.

Northeast: Active Flood Watch in NJ/MA this morning, resolving by afternoon. Normal summer conditions expected for the balance of the week. Fuel elevated (+14.0% above national) but declining.

What Dealers Should Do This Week

1. Re-run your market estimate before you post. Six weeks and -14% MoM means your May or June pricing is materially stale. The AHX Market Estimate Tool reflects current lane data — use it fresh before every post this week.

2. Enclosed carrier for high-value West Coast shipments. This is peak wildfire and heat risk week on the West Coast. Particularly for vehicles routing through Oregon and Washington — 10 Red Flag Warnings are active. A one-upgrade decision that protects against a bad outcome.

3. Take advantage of South Central and Southeast now. Zero severe alerts in both regions, cheapest fuel in the country. The window when conditions are this favorable doesn't always last — move inventory now while the execution environment is clean.

4. Get holiday-delayed shipments posted today. If you held off posting during the July 4th window, re-engage now. Carrier coverage has normalized and the market is active post-holiday.

5. Watch the Central Plains through July 12. The Flood Warnings from NWS Lincoln IL haven't lifted. Build a one-to-two-day buffer into routing through IL/KS/MO even with the overall improvement.

Frequently Asked Questions

Q: Is the six-week fuel decline going to continue, or are we approaching a floor?

A: The pace has slowed noticeably this week — WoW moves of -0.5% to -2.7% compared to last week's -1.8% to -4.8%. That's consistent with a recovery that has delivered most of its correction and is approaching a floor. We don't have enough data to say when the decline will stop, but the deceleration is a signal. The AHX Market Estimate Tool reflects current transacted lane rates in real time — more reliable for pricing decisions than directional projections.

Q: The West Coast has had a wildfire risk warning. How serious is the risk to vehicles in transit?

A: Red Flag Warnings indicate conditions are favorable for rapid fire spread — not that fires are currently burning. The risk to vehicles in transit comes from highway closures if a fire ignites on or near a major route. For standard open-carrier shipments through CA/OR/WA this week, the practical guidance is to ask your carrier to check NWS and CALFIRE/ORFIRE maps before departure and confirm routing. For high-value vehicles, the enclosed carrier option eliminates exposure to both smoke residue and routing disruption.

Q: The Central Plains flooding has been going on for six weeks. Is it finally over?

A: The dramatic improvement is real — Central Plains went from 30+ alerts last week to 6 this week. But two specific Flood Warnings from NWS Lincoln IL run through July 9 and July 12 respectively. The acute, multi-county crisis is resolved; the last lingering warnings reflect elevated river or stream levels that need more time to recede. Build a one-day buffer into routing through IL/KS/MO through July 12 as a precaution.

Q: I have vehicles I held off posting during the July 4th holiday. Is the market ready for them now?

A: Yes — the market held Carrier Market conditions through the entire holiday week and the post-holiday rebound is underway. Carrier coverage is healthy, supply is broad, and the platform is active. Post now at current market pricing using the AHX Market Estimate Tool. Well-priced shipments in this environment should book efficiently.

Q: Why has Georgia been the #1 pickup market for seven consecutive weeks?

A: Georgia's sustained top position reflects a combination of structural factors: Atlanta is one of the largest auto auction markets in the Southeast, the dealer concentration in the Atlanta metro and Georgia corridor is high, and Southeast fuel costs ($4.35/gal) make Georgia-origin lanes economically efficient for carriers. This isn't a short-term spike — it's a durable market reality that the platform data has been consistently confirming since late May.

Sign up free at autohaulerexchange.com

Data Attribution

- Diesel price data: U.S. Energy Information Administration (EIA) weekly retail diesel survey, week ending July 6, 2026.

- Weather alert data: NOAA/National Weather Service active alerts as of July 7, 2026 at 2:05 PM UTC.

- YoY comparisons reflect EIA regional diesel price data for the comparable week in 2025.

- AHX platform market environment data: Auto Hauler Exchange internal analytics, July 7, 2026.

.png)

.png)

.png)