.png)

June 23, 2026 | EIA Data: Week Ending June 22, 2026 | NWS Data: June 23, 2026 | AHX Platform Data: June 23, 2026

Four consecutive weeks. Every region in the country. The largest single-week drop of the entire reversal.

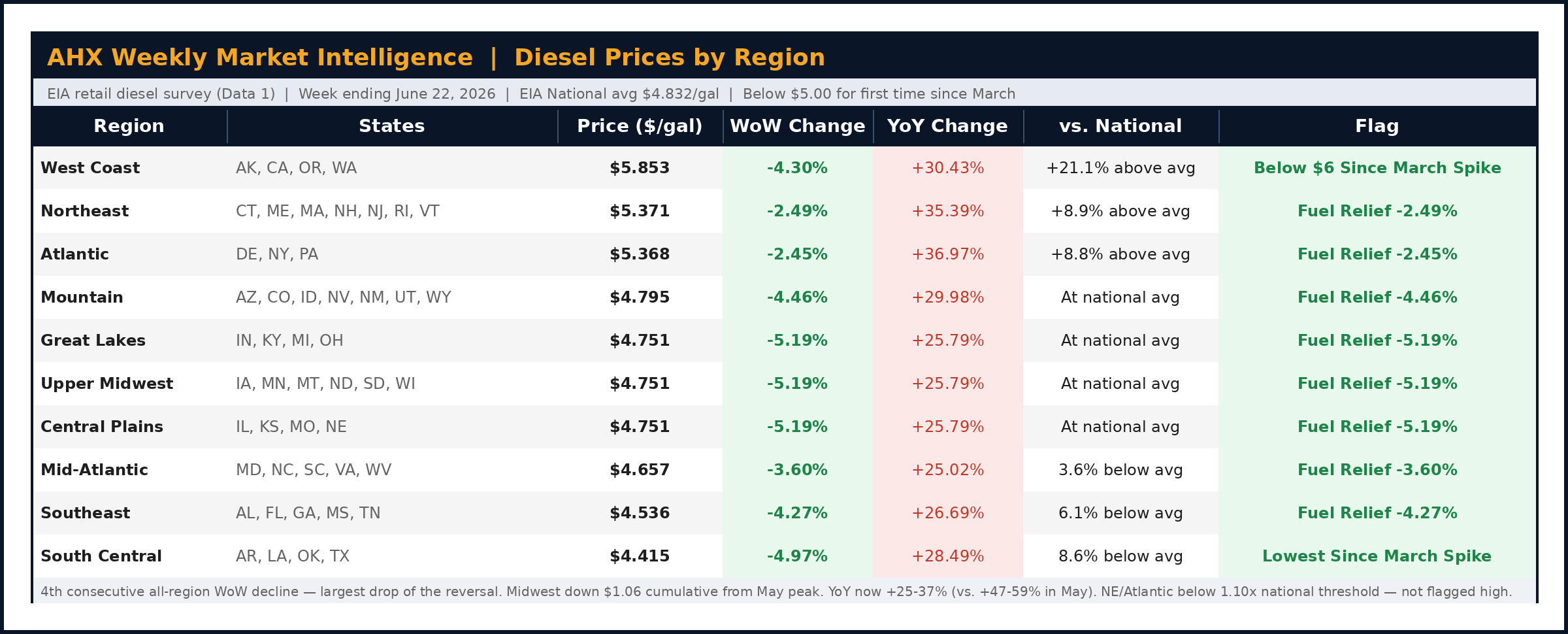

This week, the national diesel average broke below $5.00 per gallon for the first time since the spring escalation began in March. The Midwest fell -5.19% in a single week — the biggest weekly decline of the four-week fuel recovery. The West Coast crossed below $6.00 for the first time all year. South Central hit $4.415/gal — confirmed as the lowest price in that region since before the March spike.

The cumulative math from the May 11 Midwest peak: $1.064/gal recovered over six weeks — an 18.3% decline. That is not a noise event. The spring fuel crisis has reversed.

But while diesel is cooperating, the flooding situation has deteriorated significantly. The Southeast saw a major escalation this week, with 23 severe Flood Warnings active across Florida, Mississippi, Alabama, and Tennessee. And with July 4th eleven days away, the calendar is adding its own complexity.

Diesel Prices by Region — Week Ending June 22, 2026

Four Weeks Down, and the Biggest Drop Yet

The Midwest, Great Lakes, and Central Plains all fell -5.19% WoW — a single-week decline that exceeds the 5% spike threshold in reverse. The six-week cumulative Midwest decline is $1.064/gal from the May 11 peak of $5.815.

Three milestones this week:

US national average broke below $5.00. At $4.832/gal, the national average is below the $5 mark for the first time since before the March escalation. Lane pricing has been adjusting in real time — if you haven't pulled a fresh market estimate in the past week, you're working with stale numbers.

West Coast dropped below $6.00. At $5.853 on the regional average, California and the Pacific Northwest broke a threshold that held all spring and into June. Still 21% above the national average, but the trend is unmistakably lower.

South Central confirmed at lowest since March. At $4.415/gal, the Gulf Coast region is verified against the full-year EIA dataset as being at its lowest point since before the March 9 spike week — an 18.5% decline from the April 6 peak.

The YoY picture is also compressing fast: Great Lakes and Central Plains are at just +25.79% YoY, down from +47–59% in May. Any market estimate from May is meaningfully over-market. Use the AHX Market Estimate Tool before every post this week.

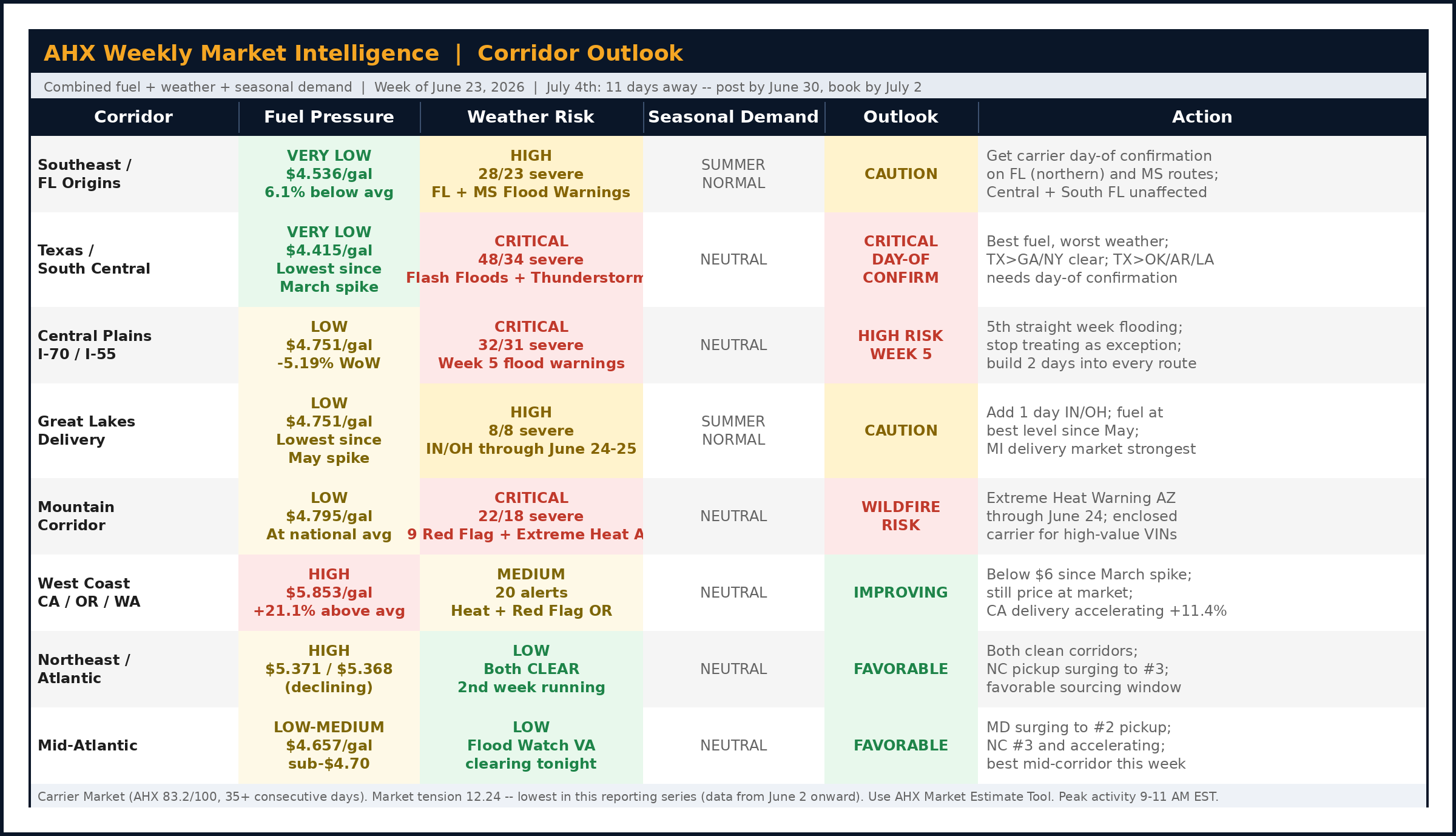

Weather Alert Summary — June 23, 2026

The Weather Story: Five Corridors, One Expanding Flood Event

South Central: Flash Floods and Severe Thunderstorms

The South Central region carries the country's highest alert load — 48 total, 34 severe. NWS Norman, OK issued Severe Thunderstorm Warnings alongside Flash Flood Warnings in Kansas and Nebraska with rainfall rates of 1.5–3 inches per hour. Carriers routing through TX, OK, AR, LA, KS, or NE need day-of confirmation before departure.

Central Plains: The Fifth Week

Sappa Creek at Oberlin, KS is running at 13.7 feet — above flood stage and above the comparable 2008 crest level. NWS St. Louis Flood Warnings run through June 25–26. Five consecutive weeks of severe flooding on I-70/I-55 means routing constraints are built-in, not exceptional. Add two days to any routing through KS, MO, or IL.

Southeast: A Major Escalation

Last week: 11 total alerts, 5 severe. This week: 28 total, 23 severe — all Flood Warnings. NWS Tallahassee covers Florida's northern corridor; NWS Jackson has warnings through June 25 in Mississippi. For the first time all season, Florida routing is genuinely compromised. FL→GA routes need carrier confirmation.

Great Lakes: All Severe

NWS Indianapolis Flood Warnings through June 24–25 — all 8 alerts rated severe. Add one day to IN/OH deliveries.

Mountain: Wildfire Steady

Nine Red Flag Warnings active. NWS Tucson Extreme Heat Warning through June 24. High-value vehicles routing through AZ or NM: consider enclosed carrier this week.

Corridor Outlook for the Week

What the AHX Platform Is Showing

The market tension score is at its lowest reading of the entire series. The Carrier Market has been in place for over 35 consecutive days. Volume is stable on the 30-day baseline and increasing week-over-week.

Georgia is the #1 pickup market on the platform for the fifth consecutive week. Maryland surged to #2; North Carolina is now #3 and accelerating. Ohio is showing simultaneous strength on pickup and delivery. Michigan leads delivery; California delivery is this week's fastest-accelerating market.

Carriers are selecting the best-priced, most straightforward shipments. Use the AHX Market Estimate Tool to anchor your posting price to current lane data, and let the AI Pricing Engine work within your range.

"Posting a shipment takes seconds. Seeing a carrier grab it in one minute shows how efficient AHX is." — Scott Moore, General Sales Manager, Suburban Volvo Cars

July 4th Is 11 Days Away

Independence Day is the largest single carrier availability dip of the summer. Carrier activity drops sharply July 3 and remains suppressed through July 6, with full normalization the week of July 7.

Post time-sensitive shipments by June 30. Target booking confirmed by July 2. If delivery timing can flex, plan for post-July 7 execution.

What Dealers Should Do This Week

- Re-run every market estimate before you post. Four weeks of fuel decline mean May estimates are meaningfully over-market.

- Plan July 4th logistics now. Post by June 30; carrier availability drops sharply July 3–6.

- Get carrier day-of confirmation on FL and MS routes. Active Flood Warnings from NWS Tallahassee and NWS Jackson — a change from recent clean weeks.

- Add two days to Central Plains routing — permanently. Five consecutive weeks of severe flooding. Build the buffer in as a baseline.

- Source from NC, MD, and GA this week. All three states show the strongest pickup carrier availability on the platform.

Sign up free at autohaulerexchange.com

Data: EIA retail diesel survey (Data 1 — All Types), week ending June 22, 2026. NWS/NOAA weather alerts as of June 23, 2026 at 3:43 PM UTC. AHX platform market environment data as of June 23, 2026.

.png)