June 2, 2026 | EIA Data: Week Ending June 1, 2026 | NWS Data: June 2, 2026 | AHX Platform Data: June 2, 2026

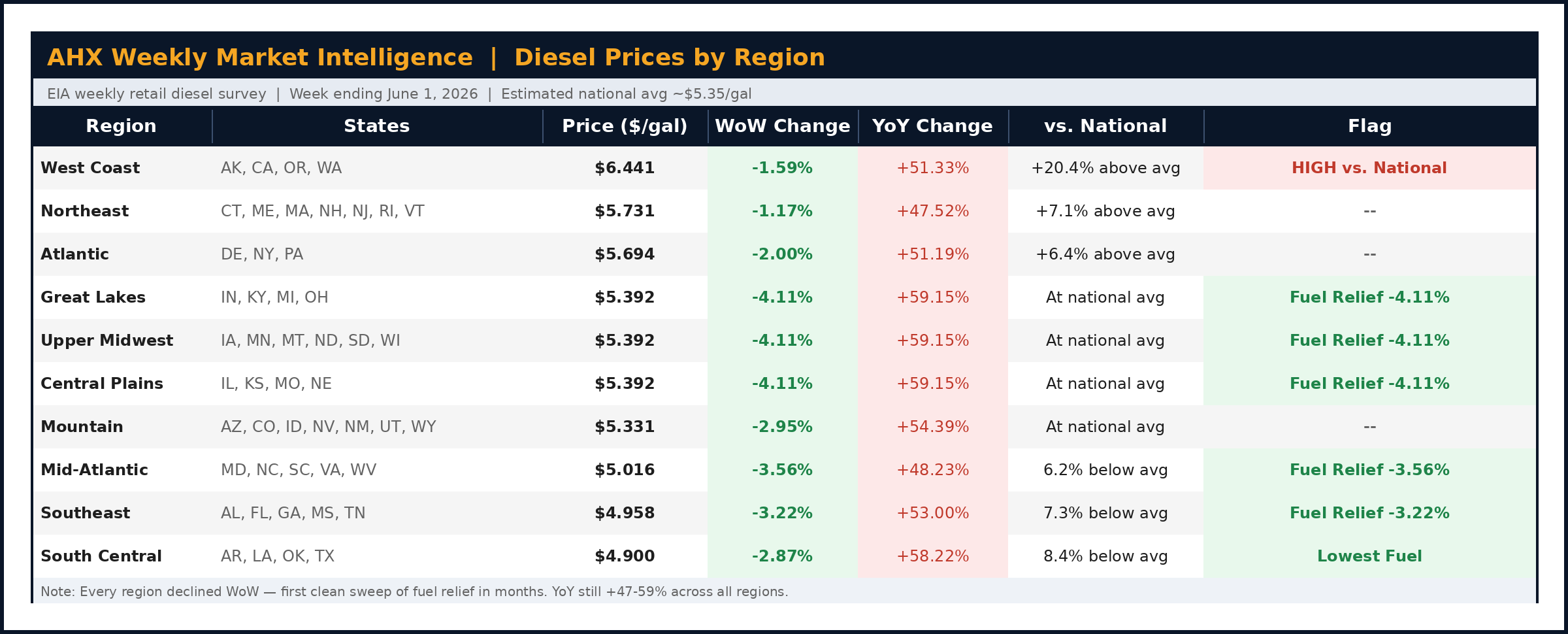

For the first time in recent memory, every single U.S. diesel region posted a week-over-week price decline. The Great Lakes, Upper Midwest, and Central Plains — which had just spiked nearly 12% in a single week as of our May 5 report — pulled back hard, dropping 4.1% in seven days. The Southeast and South Central continued their role as the country's lowest-fuel-cost corridors. Even the West Coast, stubbornly above $6.40/gal, edged slightly lower.

It looks like relief. And to some degree, it is.

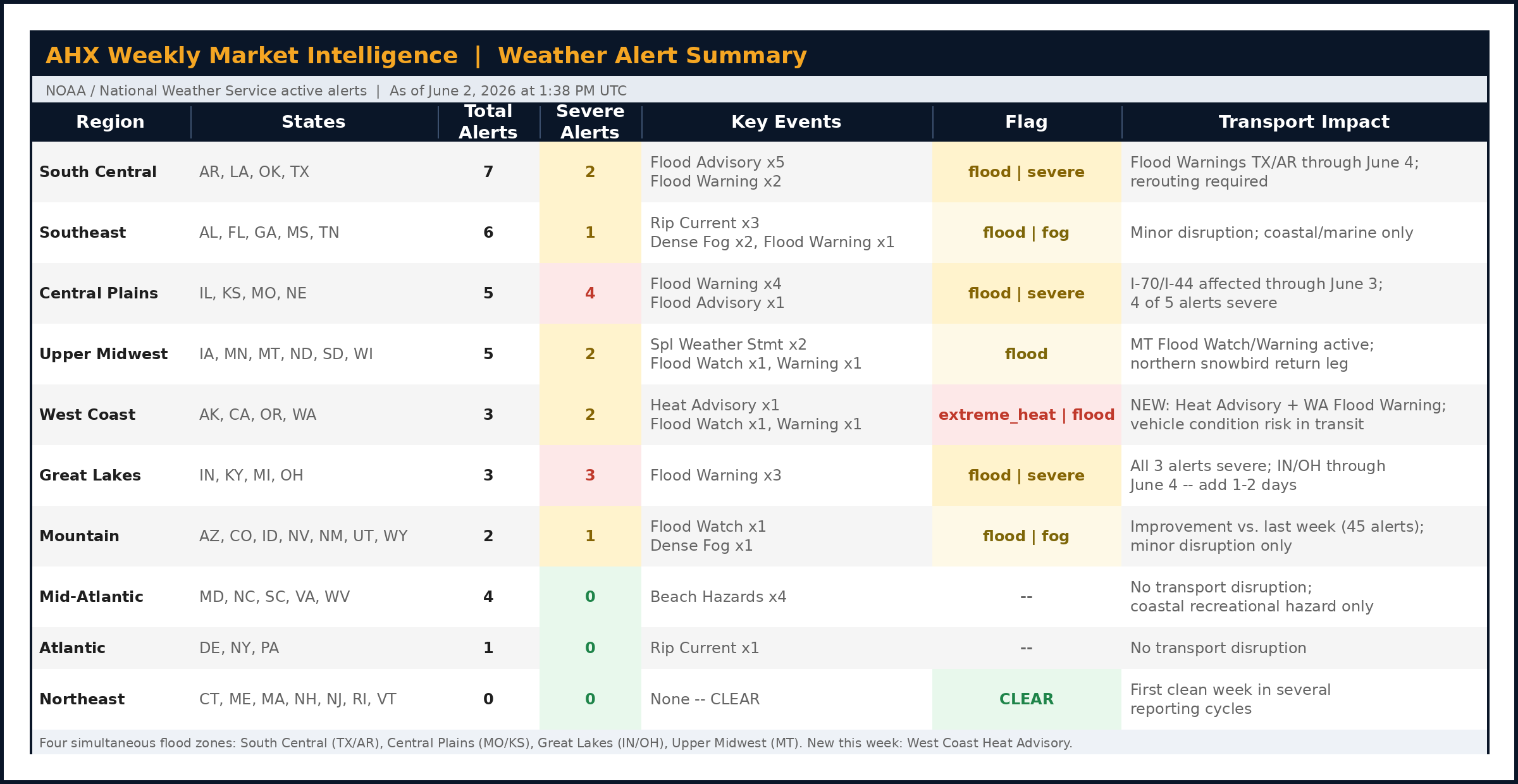

But while diesel retreated, the flooding advanced. As of this morning, active Flood Warnings and Watches are running simultaneously across South Texas, Arkansas, Missouri, Kansas, Indiana, Ohio, and Montana. Four distinct flood zones, all active at the same time. Carriers hauling vehicles through the center of the country are managing real routing constraints, and the platform data reflects it.

Here's everything you need to know this week.

Diesel Prices by Region — Week Ending June 1, 2026

The Fuel Relief Is Real — But Don't Mistake One Week for a Trend

The -4.11% WoW drop in the Great Lakes, Upper Midwest, and Central Plains is the largest single-week decline in those regions since early spring. Coming off the back of last week's nearly 12% spike, it represents a meaningful correction — likely a combination of crude market adjustments and some easing in the geopolitical premium that has kept fuel elevated since late April.

The Mid-Atlantic fell -3.56% WoW and the Southeast dropped -3.22% — broader confirmation that this isn't a regional phenomenon. For the first time in multiple reporting cycles, not a single U.S. region posted a week-over-week price increase.

Here's the important context: year-over-year, every region is still 47–59% more expensive than it was in June 2025. The Great Lakes, at $5.392/gal, is up 59.15% YoY. The South Central, the cheapest market in the country at $4.900/gal, is still up 58.22% YoY. One good week does not reset that structural reality.

The West Coast exception: California and the Pacific Northwest remain in a category of their own. At $6.441/gal — 20.4% above the national average — the West Coast diesel premium is not a weather event or a geopolitical spike. It is a structural, persistent cost reality driven by California's fuel formulation requirements, state taxes, and limited refinery alternatives. This week's data does not change that picture. Carriers running CA lanes have been operating at a massive cost disadvantage relative to the rest of the country for years.

Weather Alert Summary — June 2, 2026

Four Active Flood Zones: A Corridor-by-Corridor Look

This week's weather story isn't one event — it's four simultaneous flood zones that together cover most of the geographic center of the country.

South Central: Longest Duration, Widest Coverage

The South Central region has 7 active alerts as of this morning, including a Flood Warning running through June 4 in Corpus Christi, TX and an active warning in Arkansas. The five Flood Advisories scattered across AR, LA, OK, and TX create a wide band of compromised routing through the heart of the South Central market.

For dealers sourcing vehicles in Dallas, Houston, or San Antonio, or shipping between the Gulf Coast and the Midwest, expect carriers to be managing around closures. Texas-origin and Texas-destination shipments should build in an extra day, particularly along the Gulf Coast corridor.

The one bright spot: South Central has the cheapest diesel in the country at $4.900/gal, and the AHX platform reflects that carriers remain highly active in this market — TX→MO has 47 active carriers, TX→GA 46, and TX→TX 140. Capacity isn't the problem here; routing and timing are.

Central Plains: Highest Concentration of Severe Alerts

Missouri and Kansas are this week's highest-severity flood zone. Of the 5 alerts in the Central Plains, 4 are severe Flood Warnings — NWS Kansas City and NWS Springfield both issued warnings running through June 3. The I-70 corridor (Kansas City to St. Louis) and I-44 (Springfield area) are likely the most affected major transport routes.

If you have vehicles routing through Central Missouri this week, get specific carrier confirmation of routing before posting. The June 3 expiration of the Kansas City warning gives a clearing target — conditions should improve by midweek.

Great Lakes: All Three Alerts Are Severe

Indiana and Ohio have 3 active Flood Warnings, all three rated severe. NWS Indianapolis issued back-to-back warnings, with one extending through June 4. This is directly on the routes carriers use for Midwest auction distribution and for northbound snowbird return traffic from Florida.

Platform carrier depth in this corridor is healthy — OH→MI has 42 active carriers, MI→MO 41, PA→MI 39 — but active road closures mean those carriers are routing around conditions, not avoiding the corridor entirely. Add a day to delivery estimates and communicate that to reconditioning timelines.

Upper Midwest: Montana Active

NWS Missoula issued both a Flood Watch and a Flood Warning for Montana as of this morning. For northern snowbird return routes (FL→MN, FL→ND), the northern terminus remains unsettled — though the rest of that corridor is clear.

West Coast: New Heat Advisory

A Heat Advisory is active for the West Coast — a new flag type not present in last week's data — alongside a Flood Watch in Alaska and a Flood Warning in the Spokane, WA area. Extreme heat affects vehicle condition in transit and can influence carrier routing decisions on California-through lanes. Worth monitoring as summer temperatures build.

What the AHX Platform Is Telling Us Right Now

The data we track inside the AHX platform adds a real-time layer to everything above. Here's what we're seeing transacted right now — not industry estimates, not broker forecasts.

The market is in a Carrier Market state. That's been consistent for at least two weeks. In practical terms: carriers are active and they have options. They're selecting the best-priced, most straightforward shipments first. In a Carrier Market, pricing precision isn't optional — it's the difference between a vehicle that books today and one that sits.

The AHX Market Estimate Tool and AI Pricing Engine exist for exactly this environment. The Market Estimate Tool gives you the current lane rate based on real transacted data. The AI Pricing Engine then works within your set range to attract carriers automatically. Post at market, set a reasonable range, and let the platform do its job.

Carrier depth by lane — as of this week:

- FL→GA | FL→NY | FL→MI | FL→MO — snowbird return lanes are well-stocked right now

- TX→TX | TX→MO | TX→GA — cheap fuel is keeping carriers active in the South Central despite flooding

- CA→MO | CA→TX | CA→CA — West Coast coverage exists, but only for shipments that price for the fuel reality

- OH→MI | MI→MO | PA→MI — Great Lakes corridor carrier pools are intact; floods create routing delays, not capacity voids

One timing insight: Platform activity peaks sharply between 9–11 AM EST. That's when the highest concentration of both carriers and shippers are active on the platform simultaneously. If you're posting a shipment, do it before 9 AM so it's visible at the top of the carrier queue during peak browsing time. It matters.

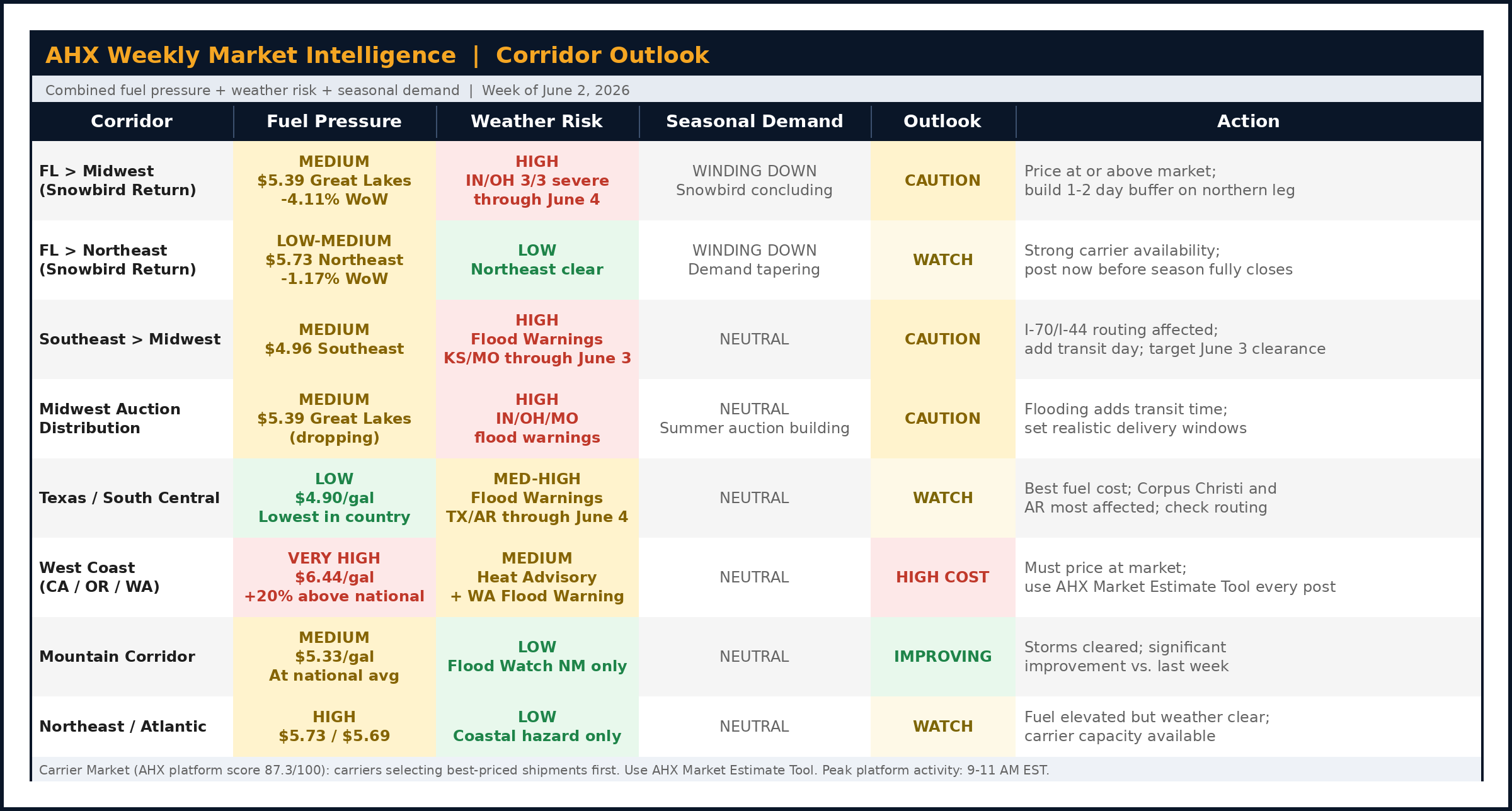

Corridor Outlook for the Week

Florida → Midwest / Northeast (Snowbird Return) Snowbird season is winding down. The northbound carrier demand surge that has compressed FL→Midwest capacity since late March is ending. But the capacity hasn't evaporated yet — there's still real depth on these lanes. The Great Lakes flood warnings (IN/OH) affect the northern leg — build in time, but don't wait. This window closes.

Midwest Auction Distribution Central Plains and Great Lakes flood conditions create routing constraints for vehicles moving between major Midwest auction hubs and dealership lots. Price at market, set realistic windows, and target June 3–4 for condition clearing on the worst-affected routes.

West Coast Acquisitions At $6.441/gal — 20% above the national average — California and Pacific Northwest lanes require carrier pricing that reflects the fuel reality. With carriers active on CA→CA and on CA→MO, the coverage is there for shipments priced correctly. Always run the AHX Market Estimate Tool before posting a West Coast shipment.

Southeast and South Central: Best Fuel, But Watch Routing The Southeast ($4.958) and South Central ($4.900) are the cheapest diesel markets in the country. Carrier cost basis on Florida, Texas, and Gulf Coast lanes is the most favorable it's been in months. Active Flood Warnings in Texas and Arkansas mean routing matters — but the deep carrier pools in this market mean vehicles can move if they're priced right.

Industry Context: Summer Transition and Pricing Dynamics

We're entering the summer market transition. A few dynamics worth watching:

Used vehicle pricing: Average marketed prices have been running around $51,000–$51,500 this spring. Summer historically brings some moderation as the spring demand surge fades. Dealers who have been slow to replenish inventory due to transport cost concerns may find early summer a reasonable window to move on acquisitions, particularly now that diesel is pulling back from the May spike levels.

Snowbird volume tapering: The FL→Midwest and FL→Northeast northbound volume surge is ending. Plan your Q3 transport budget with lower northbound FL volumes as the baseline.

What Dealers Should Do This Week

1. Move Midwest and Central Plains shipments with realistic windows. Active Flood Warnings in Indiana, Ohio, and Missouri run through June 3–4. Add one to two days to your expected delivery timeline. Communicate this to reconditioning and retail scheduling.

2. Price California and Pacific Northwest lanes at current fuel reality. At $6.441/gal — 20% above the national average — West Coast lanes priced at generic market rates will sit. Use the AHX Market Estimate Tool to see current transacted lane rates before posting.

3. Take advantage of the Florida northbound window now. Snowbird season is ending. Carrier availability on FL→Midwest and FL→Northeast lanes is at its best point in three months. With 67 carriers active on FL→GA alone, the depth is there — but it won't last. Post your Florida acquisitions this week.

4. Post in the morning. Platform activity peaks 9–11 AM EST. Post before the morning rush starts so your shipment is at the top of the queue when carriers are most active.

5. Check your summer transport budget against real fuel data. The 47–59% YoY diesel premium has been persistent all year. When building your Q3 transport budget, do not use pre-2025 cost baselines. The structural fuel cost environment has shifted.

Frequently Asked Questions

Q: Diesel dropped this week everywhere — does that mean vehicle transport rates are coming down?

A: Week-over-week fuel relief is real, but transport lane rates adjust more slowly and reflect more than just diesel. Carriers factor in their fixed costs, equipment financing, and the cumulative YoY fuel cost that has been 47–59% above last year all spring. Expect a gradual easing over several weeks, not an immediate reset. Use the AHX Market Estimate Tool to see real transacted lane rates rather than estimating from fuel data alone.

Q: How long will the flooding affect Midwest and Central Plains shipments?

A: The most severe active Flood Warnings in Indiana, Ohio, and Missouri are dated through June 3–4, 2026 per current NWS advisories. The South Central (Corpus Christi) warning also runs through June 4. Barring new storm systems, conditions should begin clearing mid-week. Add one to two days to any affected routes and monitor NWS for updates.

Q: Why is California diesel so much more expensive than the rest of the country?

A: California diesel runs 20% above the national average ($6.441 vs. ~$5.35 national) due to California-specific fuel formulation requirements (CARB standards), state and local fuel taxes among the highest in the country, and limited refinery capacity relative to demand. This is not a temporary spike — it is a structural cost premium built into the carrier cost structure on all CA-touching lanes. Always use the AHX Market Estimate Tool before posting a West Coast shipment.

Q: Is snowbird season over? How does that affect my FL acquisitions?

A: Snowbird season — the annual migration of retirees shipping vehicles north from Florida, Arizona, and the Carolinas — wraps in early June. The northbound carrier demand surge that compressed FL→Midwest capacity since late March is ending. AHX platform data shows strong depth right now that will normalize as the season concludes. If you have FL acquisitions waiting, this week is a better window than mid-June.

Q: The market is described as a "Carrier Market" — what does that mean for me as a dealer shipper?

A: A Carrier Market means carriers have enough options that they can be selective. They will pick up the shipments that are priced at market rate, are easy to schedule, and have clean pickup/delivery instructions. Shipments priced below market, or posted with vague logistics, get passed over first. The practical fix is straightforward: use the AHX Market Estimate Tool to anchor your price to current lane data, and let the AI Pricing Engine work within your range to attract the right carrier. Price at market and the platform moves fast. Price below it and you're competing in a market that isn't in your favor right now.

Q: Should I be worried about the Heat Advisory on the West Coast for vehicle shipments?

A: Heat Advisories can affect open-carrier shipments, particularly for vehicles with dark paint or temperature-sensitive electronics. For high-value vehicles, consider enclosed carrier options when extreme heat conditions are active. For standard open-carrier shipments, the primary impact is on carrier routing efficiency — transit time may stretch slightly during extreme heat events on California and Pacific Northwest lanes.

Sign up free at autohaulerexchange.com

Data Attribution

- Diesel price data: U.S. Energy Information Administration (EIA) weekly retail diesel survey, week ending June 1, 2026. Published June 2, 2026.

- Weather alert data: NOAA/National Weather Service active alerts as of June 2, 2026 at 1:38 PM UTC.

- YoY comparisons reflect EIA regional diesel price data for the comparable week in 2025.

- AHX platform market environment and lane supply data: Auto Hauler Exchange internal analytics, as of June 2, 2026.

.png)