Before we get into diesel prices and weather alerts, let's start with the market signal that should be on every dealer's radar this week: Florida outbound is now the most imbalanced state in the AHX network by a wide margin — over 11 vehicles leaving for every one coming in, with outbound pricing running 162% higher than inbound. That's not a seasonal blip. It's a structural capacity squeeze, and dealers who don't price for it will sit unbooked.

Combined with diesel costs plateauing at +65% year-over-year in the Midwest, active flooding in the Central Plains entering week four, and a new heat wave hitting the Northeast — this week's transport market has a lot for dealers to navigate.

AHX Marketplace Conditions: The 30-Day Network View

Demand is up sharply across the board. The average rate per mile on the AHX network is up 34% YoY.

Translation for dealers: capacity is tighter than it was a year ago, freight is moving faster, and you're going to feel it most in a handful of states where vehicles are flowing out in volume.

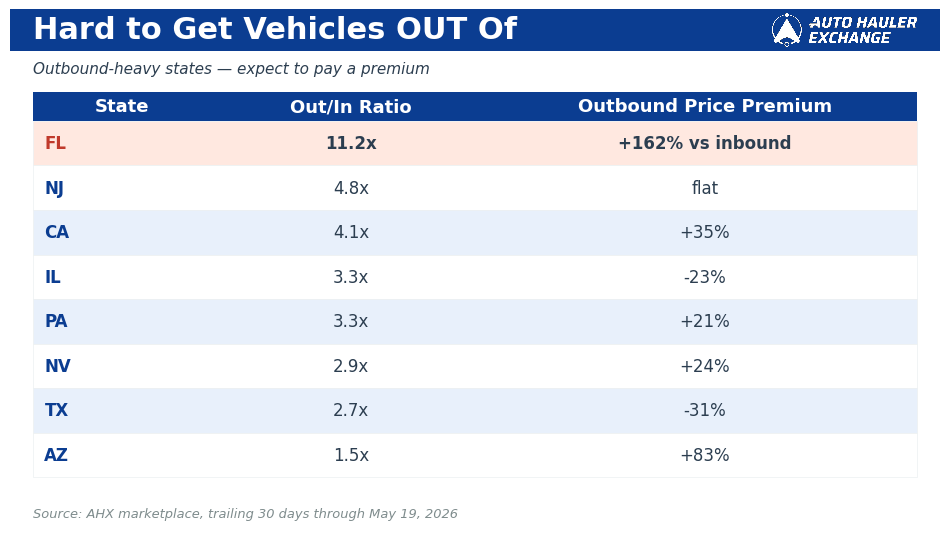

State of the Map: Where the Imbalance Is

The metric that matters for dealers isn't volume alone — it's the ratio of vehicles leaving vs. arriving, because that's what drives what you'll pay to move metal.

Florida is the standout. It's the most imbalanced market in our network by a wide margin — over 11 vehicles leaving for every one coming in, with outbound pricing 162% higher than inbound. Dealers shipping out of FL should expect to pay a real premium and post earlier than usual to give carriers time to reposition.

California, Arizona, and New Jersey are the other tight outbound markets to watch — all showing meaningful outbound price premiums driven by the same dynamic.

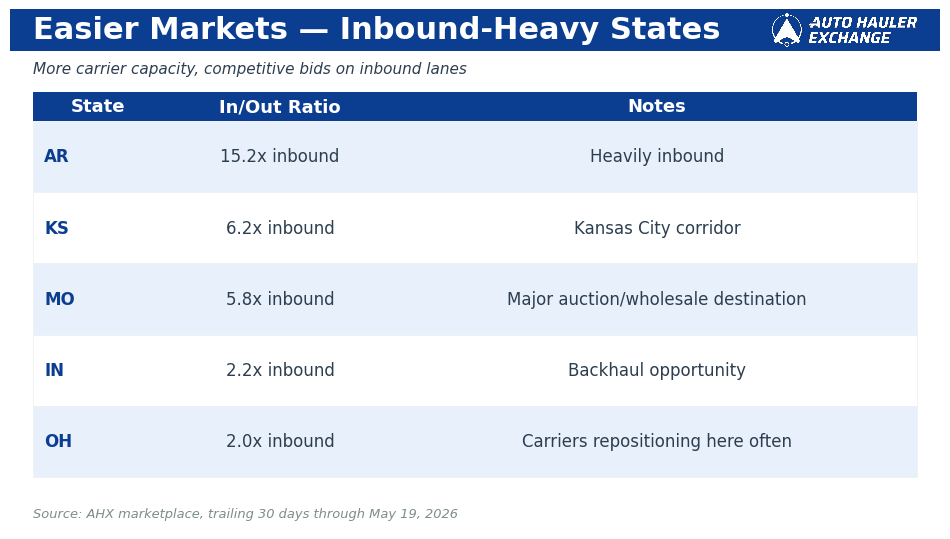

Easier markets (inbound-heavy, more carrier capacity)

Dealers buying inventory and bringing it into the Midwest are in the strongest position. Carriers are actively repositioning into MO/KS/OH/AR, which means more capacity and competitive bids on inbound lanes.

The Fuel Situation: Midwest Diesel Plateau, Mountain Rising

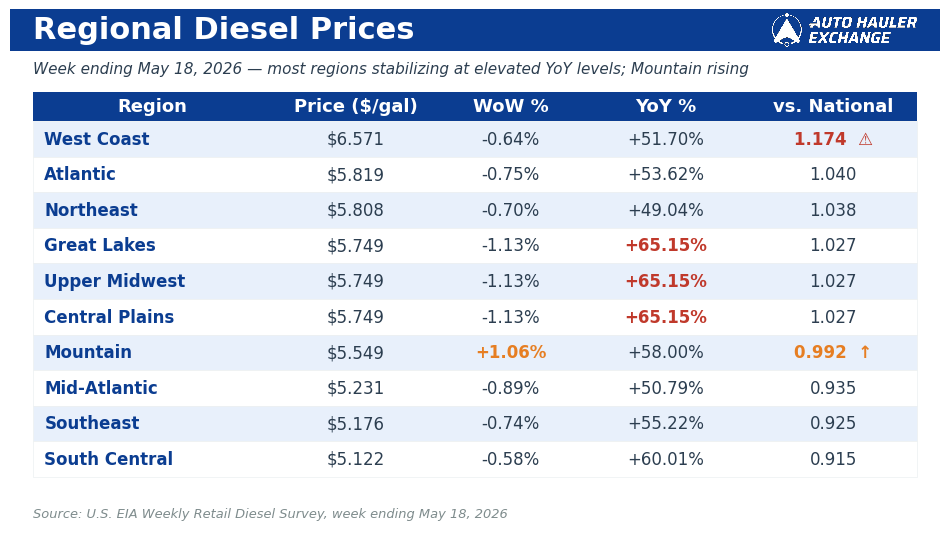

Last week's single biggest story was a diesel shock in the Midwest — Great Lakes, Upper Midwest, and Central Plains all jumped +11.91% in one week to $5.742/gal, the sharpest regional spike we'd tracked in months. This week's EIA data (survey week ending May 18, 2026) delivers an important update: those three regions are now at $5.749/gal — essentially unchanged.

That's not good news. A plateau at the top of a spike is not recovery. Carriers on Midwest lanes absorbed an 11.9% cost increase last week, and they haven't gotten any relief this week. The year-over-year figure tells the real story: Great Lakes, Upper Midwest, and Central Plains diesel is running +65.15% above where it was one year ago. That's the highest YoY reading in the country.

The one region bucking the broad stabilization trend: Mountain, which rose +1.06% WoW to $5.549/gal. At 99.2% of the national average, it's not yet flagged as "high vs. national," but it's the only region moving in the wrong direction this week — and it's doing so against a backdrop of active wildfire conditions (more on that below). If Mountain follows the same pattern as last week's Midwest, a more significant move next week is possible.

The rest of the picture: most regions showed modest week-over-week relief, ranging from -0.58% (South Central) to -1.13% (Great Lakes/Upper Midwest/Central Plains). West Coast remains the structural outlier at $6.571/gal — 17.4% above the national average — with essentially no movement week-to-week.

The key takeaway for dealers: broad fuel stabilization at elevated levels is not the same as fuel prices coming down. Carrier base costs remain dramatically higher than one year ago across every region in the country. Posted prices that don't reflect that reality will sit unbooked.

The Weather Picture: Four Weeks of Flooding and a New Heat Wave

Central Plains: The Country's Most Operationally Compromised Corridor

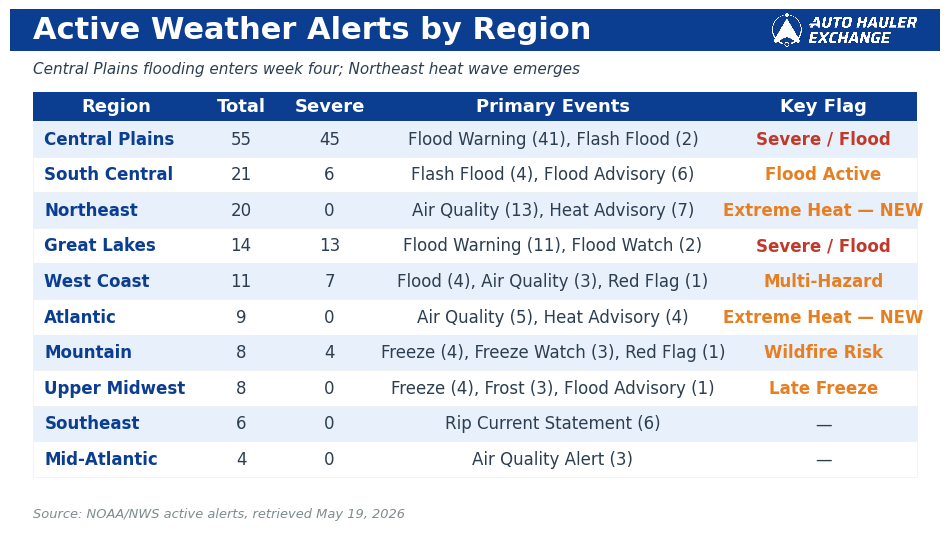

For the fourth consecutive week, the Central Plains corridor (IL, KS, MO, NE) is the most weather-impacted region in the country. This week's numbers: 55 active weather alerts, 45 of them severe-rated. The dominant event type: Flood Warnings (41 active), with additional Flash Flood Warnings (2), Flood Watches (3), and Hydrologic Outlooks (4).

NWS Paducah KY and NWS Springfield MO issued multiple Flood Watches and Warnings extending through Tuesday and Wednesday. For carriers routing through IL, MO, and NE, detour requirements are not theoretical — they're operational. Transit time estimates on Central Plains lanes should include a 1-3 day buffer this week.

This compounds the AHX marketplace signal: MO/KS are already the highest-demand inbound destinations in our network. Adding active flooding to already-tight inbound capacity means dealers buying into Kansas City should expect to pay carriers for the operational difficulty, not just the miles.

Great Lakes: Still Severe

Great Lakes (IN, KY, MI, OH) carries 14 active weather alerts, with 13 of those rated severe — almost entirely Flood Warnings. NWS Indianapolis has Flood Warnings active through 8AM EDT Wednesday, May 21, and one extending all the way to 2AM EDT Saturday, May 23. That Saturday warning is worth noting: it extends through Memorial Day weekend setup.

The New Development: Northeast Heat Wave

This is the weather story that wasn't on anyone's radar last week: Heat Advisories are now in effect across the Northeast and Atlantic, with 20 total weather alerts in the Northeast region (13 Air Quality, 7 Heat Advisory) and 9 in the Atlantic (5 Air Quality, 4 Heat Advisory).

NWS Upton NY and NWS Mount Holly NJ both issued Heat Advisories running through 8PM EDT Wednesday, May 20. This matters for dealers shipping vehicles on open carriers to the New York, New Jersey, and New England markets. Extreme heat can affect vehicle condition during transit, and some carriers reduce operating pace in heat events.

Mountain: Unusual Dual Pressure

The Mountain corridor is running an unusual combination this week: four Freeze Warnings and three Freeze Watches (from NWS Cheyenne WY, active through Tuesday morning) alongside a Red Flag Warning indicating active fire weather conditions. Cold nights, dry and windy days — a pattern consistent with mid-May in the Mountain West, but worth monitoring for CO, WY, and NM lane disruptions. Combined with the week's only upward fuel move (+1.06%), Mountain is the region to watch heading into next week.

What Dealers Should Do This Week

1. If you're shipping out of Florida, post earlier than usual and price at or above market. Florida outbound is the most capacity-constrained lane in the country right now. With 11.2 vehicles leaving for every one arriving, carriers have to deadhead in or reposition empty, and they're pricing accordingly. Postings at last month's rates will sit. Use the AHX Market Estimate Tool to set a price that reflects what carriers are actually accepting today.

2. Price Midwest-corridor postings at market — and account for fuel. Great Lakes and Central Plains carriers are absorbing diesel costs that are +65% YoY. Combined with active flooding adding 1-3 days of transit buffer, posted prices need to reflect both pressures. The AHX Market Estimate Tool pulls real-time market data so your posted price reflects current conditions, not what carriers were accepting when fuel was 65 cents a gallon cheaper.

3. Post pre-Memorial Day vehicles by Wednesday, May 21. Memorial Day weekend is seven days away. Carrier availability drops over holiday weekends — consistently. If you have vehicles that need to move before the holiday or during it, the window to book a carrier with certainty closes around Wednesday. Tuesday is the fastest day to post overall (63.6 hrs to book on average vs. 119 hrs for Friday posts), so Tuesday morning is the sweet spot this week.

4. Flag Northeast open-carrier shipments for vehicle condition. Heat Advisories are active in the NJ, NY, and New England markets through Wednesday evening. For high-value pre-owned vehicles or units with known electronics or HVAC sensitivities, it's worth considering whether enclosed transport is more appropriate for this window. For standard open-carrier shipments, set dealer expectations that carrier pace may be slightly reduced in extreme heat.

5. If you're buying inventory into the Midwest, capacity is in your favor. Carriers are actively repositioning into MO, KS, OH, and AR — the inverse of the Florida problem. AR is running 15.2x inbound, KS 6.2x, MO 5.8x. You should see competitive carrier bids on inbound lanes into these markets. The flooding adds operational friction, but the underlying capacity dynamic favors buyers.

6. Be vigilant for transport fraud heading into Memorial Day weekend. Holiday weekends bring a measurable spike in transport fraud attempts. Fraudsters bank on dealers being busy and letting verification processes slide. Don't skip carrier vetting — verify insurance, confirm DOT authority, and trust your gut if something feels off.

With 5,500+ vetted carriers, one-day average time from posting to carrier booking, and real-time ELD tracking on every active shipment, AHX gives you the tools to move faster than the market.

Frequently Asked Questions

Q: Why is Florida outbound so much more expensive than Florida inbound right now? A: Carriers price for the round trip, not the single leg. When 11 vehicles leave Florida for every one arriving, carriers either deadhead in empty or reposition from another state — and they need to recover that cost somewhere. They recover it in the outbound rate. Until inbound flow normalizes (late spring/early summer typically helps as snowbird migration tapers), FL outbound dealers should expect to pay a structural premium.

Q: Midwest diesel is +65% year-over-year. Does that mean transport rates on Midwest lanes are also 65% higher than last year? A: Not directly — carrier rates don't move 1-to-1 with diesel prices because fuel is only one component of carrier operating costs. But elevated fuel costs do put sustained upward pressure on carrier rate expectations, especially on lanes where carriers are already running at thin margins. The +65% YoY figure means Midwest carriers are absorbing significantly higher base costs than a year ago, and they're pricing accordingly. The right approach is to use real-time market data (like the AHX Market Estimate Tool) rather than benchmarking against rates from 12 months ago.

Q: Central Plains has been flooded for four weeks straight. At what point does persistent flooding create long-term carrier capacity changes? A: Sustained weather disruptions in a region can gradually shift carrier routing patterns — carriers learn to avoid certain corridors or charge more to operate on them. After four weeks of active flooding on IL/MO/NE routes, some carriers may already be pricing in a disruption premium on Central Plains lanes. The practical implication: don't assume that what you paid to move vehicles through this corridor in March reflects current market rates.

Q: Why does Mountain being the only region with rising fuel matter if it's still below the national average? A: Directional trend matters as much as absolute level. Mountain diesel is rising while every other region is flat or declining. If this continues for 2-3 more weeks and Mountain crosses the national average — or spikes the way Midwest did last week — it creates cost pressure on AZ/CO/NV/UT/WY lanes that isn't currently priced in. Watching the direction early gives you time to adjust your posting strategy before it becomes a problem.

Q: Does posting on Tuesday vs. Friday really make that big a difference? A: Yes — and the data is consistent. The average AHX load posted on Tuesday books in 63.6 hours. The same load posted on Friday takes 119 hours, nearly twice as long. Carriers browse the load board most heavily Monday morning, so posts that are already live by 9 AM EST Monday catch the peak browsing window. The practical takeaway: if you have any flexibility in when you post, Monday-Tuesday is the high-leverage window.

Q: Memorial Day is one week out. What's the practical carrier availability impact? A: Holiday weekends reliably reduce carrier availability for 2-4 days. Memorial Day is particularly impactful because it's a three-day weekend and many carriers take 4+ days off. The practical window: post vehicles you need moved before or during the holiday by Wednesday, May 21. Postings that go live Thursday or Friday of next week will face meaningfully thinner carrier interest through the weekend.

Sign up free at autohaulerexchange.com

Data Attribution: Diesel prices: U.S. EIA Weekly Retail Diesel Survey, survey week ending May 18, 2026, published May 19, 2026. Weather data: NOAA/NWS active alerts, retrieved May 19, 2026 at 16:53 UTC. AHX marketplace data: trailing 30 days through May 19, 2026, derived from booked loads with confirmed pickup/delivery locations.

.png)

.png)

.png)